Introduction

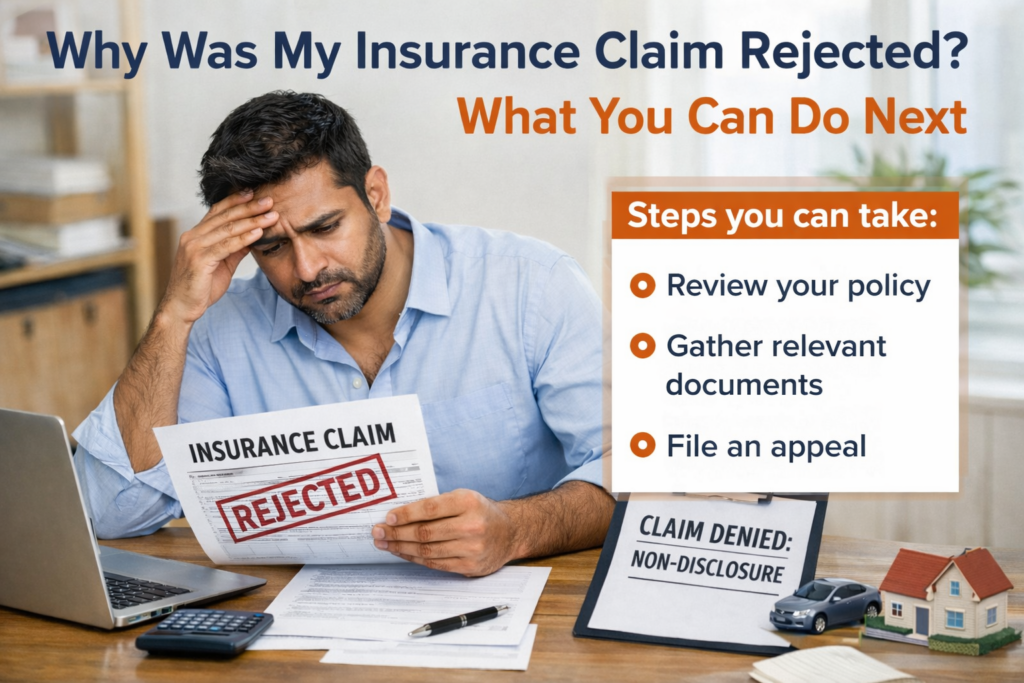

“Your medical claim is rejected due to a pre-existing disease.”

This is perhaps the most frustrating message that a policyholder can receive. One buys health insurance to feel secure about their finances in any medical emergency, but when they actually need it, the insurance company rejects it. Most people do not even know what “pre-existing disease” is or how it is being applied to them.

Pre-existing disease

Pre-existing disease refers to any illness, condition, or symptom that a person may have had before they purchased the insurance policy.

Insurance companies normally apply this reason to reject claims, sometimes even without any valid reason. The good news is that rejection does not necessarily mean that the insurance company is correct. There are some rules and steps that can be followed to challenge such rejections.

Why Medical Claims Are Rejected on the Ground of Pre-Existing Disease?

The medical claims are rejected on the grounds of pre-existing disease, primarily due to the waiting period. The waiting period for pre-existing diseases in most health insurance policies is between 2 to 4 years.

The reasons for rejection of the claim are as follows:

The disease was present before the purchase of the policy, and the waiting period was not served

The disease was not disclosed at the time of purchasing the policy

The medical records indicate that the treatment was previously sought for the same disease

The hospital has mentioned the history in the discharge summary

What Insurers Typically Say?

When denying such claims, insurers typically say:

“The disease existed before the inception of the policy”

“The policyholder did not disclose his/her medical history”

“The treatment is related to a pre-existing condition”

“Waiting period clause applies”

Such statements seem conclusive, but they are not necessarily correct.

What Steps Can Be Taken After Medical Claim Rejection?

Step 1: Read the Rejection Letter Carefully

Do not panic. Read the rejection letter carefully and understand the reason for rejection. Check:

Policy clause number

Waiting period mentioned

Medical condition they are calling pre-existing

Step 2: Check Your Policy Document

Check the following in your policy document:

Date of your policy

Waiting period for pre-existing diseases

Whether the disease was disclosed in the proposal form

If the waiting period is already over, it is likely that the rejection is not correct.

Step 3: Collect Medical Records

Collect the following medical documents:

Old prescriptions

Diagnostic reports

Doctor’s notes

Hospital discharge summary

Check if the current treatment is actually related to the alleged pre-existing disease.

Step 4: Request Clarification in Writing

Email the insurance company and request:

How the disease is pre-existing

Medical evidence used

Policy provision to reject the claim

Always do this in writing.

Step 5: Make a Complaint to the Insurer

If the explanation is not satisfactory, make a complaint to the insurance company’s grievance cell. Attach all documents and state your case clearly in simple language.

Step 6: Take the issue further to an Insurance Ombudsman

If the insurance company does not reach out to you within the timeframe of 30 days, you can take your complaint to the Insurance Ombudsman. This is completely free and consumer-friendly. Many policyholders have received their claim after it was rejected at this stage.

Legal Assistance

The IRDAI regulations ensure that the policyholder is not treated unfairly in the rejection of claims. According to the IRDAI regulations:

Pre-existing conditions should be defined properly

The waiting period cannot be extended unfairly

Claims cannot be rejected without valid medical evidence

The courts have also stated that just an allegation of pre-existing conditions is not sufficient to reject any claims.

How to Avoid Such Rejection in the Future?

Always disclose medical history honestly

Keep copies of proposal forms

Buy insurance early in life

Renew policy without breaks

Read waiting period clauses carefully

Conclusion

A denial of a medical claim on the grounds of pre-existing conditions can be very disappointing, more so when one is already burdened with medical bills and recuperation. However, a denial of a medical claim based on pre-existing conditions does not mean that the insurance company has valid grounds to deny your claim. In most cases, such denials are based on certain presumptions, a lack of adequate medical knowledge or simply because the insurance company is acting within the terms and conditions of the policy.

A policyholder has the right to question and ask for a written explanation of the reasons for denial, if it deems unjust, and also file a grievance against such unjustified denial both with the insurer’s grievance mechanism and with the Insurance Ombudsman. That process is meant for consumer protection, and it’s not as tough as many might think. Health insurance is meant to be a source of strength in times of need, and being informed and proactive will ensure that your health insurance policy is working for you when it counts the most.

This article is developed with research support from Akanksha Singh under the guidance of Advocate Srilatha and Advocate Niranjan Reddy, experienced legal professionals at Black Legal Associates with substantial experience across diverse legal matters. For legal assistance, contact 8500096262.