Introduction-

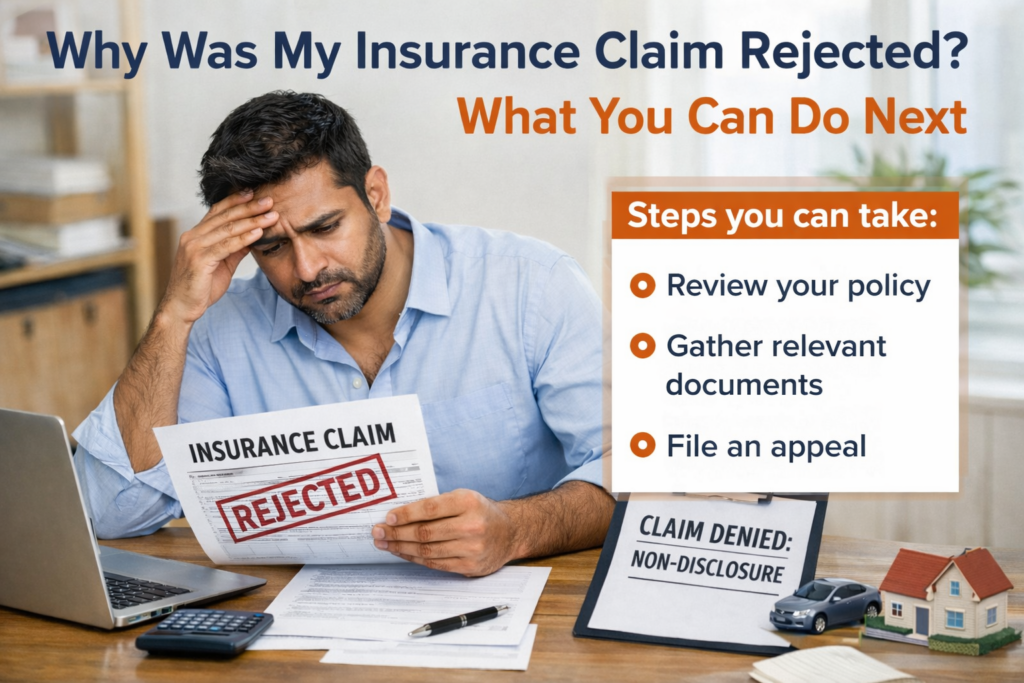

Insurance claim rejection is stressful, especially when the reason mentioned is “non-disclosure of facts.” Many policyholders feel cheated because they genuinely believe they told the insurance company everything important. This blog explains, in simple terms, what non-disclosure means, why insurance companies reject claims on this ground, and what practical steps you can take if your insurance claim is rejected for non-disclosure.

What Does Non-Disclosure Mean In Insurance?

Non-disclosure means not sharing important information with the insurance company at the time of buying the policy. Insurance works on trust. The company decides the premium and coverage based on the details you provide in the proposal form.

For example:

A previous illness not mentioned in a health insurance form

A past accident or modification not disclosed in motor insurance

Smoking or alcohol habits hidden in life insurance

Why Do Insurance Companies Reject Claims For Non- Disclosure?

Insurance companies usually reject claims for non-disclosure because they believe the hidden information would have changed their decision to insure you or affected the premium amount.

Common reasons given by insurers include:

The policyholder did not disclose a pre-existing disease

Medical history was incomplete or incorrect

Previous insurance claims were not mentioned

Material facts were deliberately concealed

Most rejection letters contain technical language, but the meaning is usually simple. They often say that the policyholder violated the ‘duty of disclosure’ or provided false information while purchasing the policy.

They may also mention that if the correct facts were disclosed, the policy would either not have been issued or would have been issued on different terms.

Is Every Non-Disclosure Valid Ground For Rejection?

No.This is very important for policyholders to understand. Not every non-disclosure automatically justifies claim rejection.

A claim can be challenged if:

The non-disclosed fact had no connection with the claim

The policyholder was not asked a specific question about it

The omission was unintentional or due to lack of knowledge

The insurer failed to conduct proper checks at policy issuance

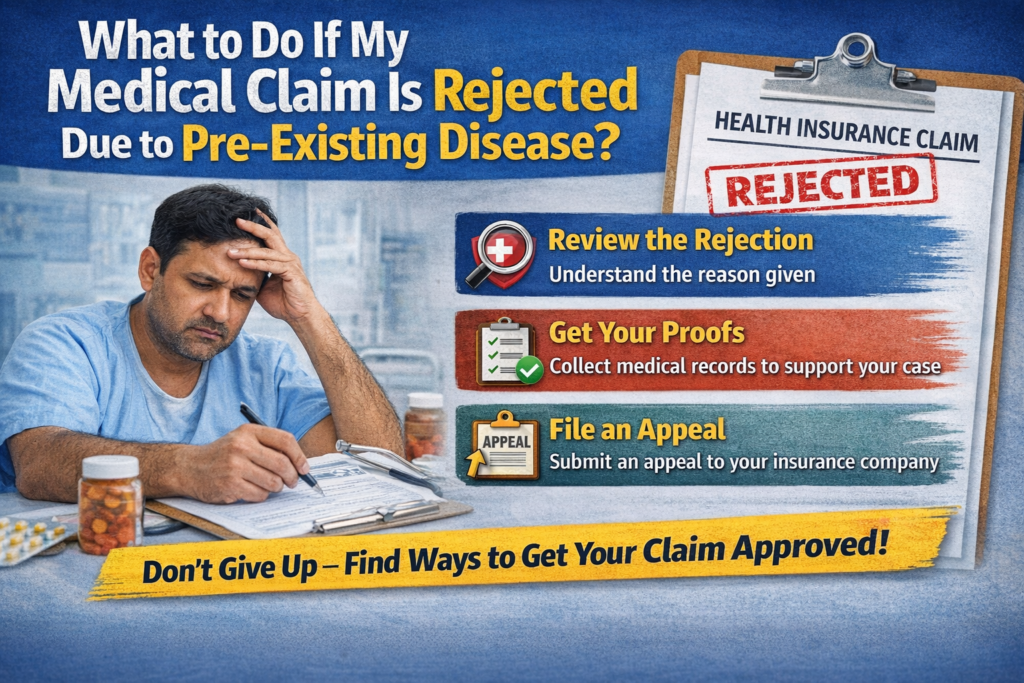

Practical Steps to Take if Your Claim Is Rejected for Non-Disclosure-

Read the Rejection Letter Carefully

Check exactly what information the insurer claims was not disclosed. Compare it with your proposal form and documents submitted at the time of policy purchase.

Check the Proposal Form You Filled

Many policyholders do not fill proposal forms themselves.Agents often do it. If incorrect information was filled by the agent without your knowledge, you may not be at fault.

See If the Non-Disclosure Is Related to the Claim

If the rejected claim has no link to the alleged non-disclosure, you have strong grounds to challenge the rejection. For example, rejecting an accident claim due to an unrelated past illness can be unfair.

File a Written Representation with the Insurer

Write to the insurance company asking for a detailed explanation and submit supporting documents. Keep copies of all emails and letters.

Escalate to the Insurance Ombudsman

If the insurer does not resolve the issue, you can approach the Insurance Ombudsman. This is a free and policyholder-friendly forum designed to resolve insurance disputes.

Approach the Consumer Commission

If the claim amount is significant, filing a complaint before the Consumer Commission is another effective remedy. Many consumers have received relief in non-disclosure cases.

Legal Support-

Indian law does not allow insurance companies to reject claims casually by simply stating non-disclosure. Courts and consumer forums have consistently held that only material non-disclosure can be a valid ground for rejecting an insurance claim. This means the undisclosed information must be important enough to influence the insurer’s decision while issuing the policy and must have a direct connection with the claim raised. Minor, unrelated, or trivial omissions cannot be used to deny a genuine claim, especially when the undisclosed fact has no bearing on the loss or illness for which the claim is made.

Another important legal protection relates to proposal forms. In many cases, insurance agents fill out the forms on behalf of policyholders. Consumer forums have repeatedly ruled that if incorrect or incomplete information was recorded by the agent, or if the questions were vague and poorly explained, the insurer cannot take advantage of its own agent’s error to reject a claim. Insurance companies are legally responsible for the acts of their agents, and policyholders cannot be penalised for mistakes they did not knowingly make.

Conclusion

A claim rejection for non-disclosure is not the end of the road. Many such rejections are overturned when challenged properly. Always read rejection letters carefully, check your proposal form, and take timely action. Insurance is meant to provide financial security, and policyholders have rights when claims are unfairly denied.

This article is developed with research support from Anushka Tiwari under the guidance of Advocate Srilatha and Advocate Niranjan Reddy, experienced legal professionals at Black Legal Associates with substantial experience across diverse legal matters. For legal assistance, contact 8500096262.